|

| Conference in a new format: Some venues are switched via video. An enormes increase in outreach. (Source: Corporate Group Maleki) |

In this times when

political Europe is becoming more and more divisive, the financial

industry is trying to save from common European projects what can be

saved. To support this process, a new format is being created, the

conference Future Europe. The Maleki Corporate Group has organized a

simultaneous conference. Participants at several European places were

also able to make their contributions in Frankfurt, Amsterdam, Paris

and London. The forum, with top class participants at all locations,

successfully completed its entry. The event is supposed to be

continued every six months.

The welcome speach

was held by Dr. Andreas Dombret, until recently board member of the

Deutsche Bundesbank, to all participants. This format would come at

the right time. What started on European initiatives for a common

financial market must be brought to an end. Thus, after the launch of

the banking union, now capital market union must be addressed. It

should be decided whether this should happen with or without Great

Britain. Dombret cautiously points out the need to share liabilities

in Europe as well.

|

| Dr. Andreas Dombret adresses to the audiance (Source: Thomas Seidel) |

Via a recorded

speech Peter Praet, chief economist of the European Central Bank

(ECB), warned that the banks' traditionally national ties were

another risk factor. This would hamper the creation of a true common

financial market in Europe. It is urgent to find a European solution

for a guarantee of customer deposits. In the event of a bank

collapse, it would be unavoidable in the future to involve the

taxpayer as an indirect guarantor.

Financing Europe's economy

After these

speeches, the first panel will start, titled "Financing the EU

Economy". Philippe Oddo, head of the French ODDO Bank, which not

long ago bought up the traditional German BHF Bank from Deutsche

Bank's portfolio, justified his commitment to gaining expertise in

the German market. Oddo believes that the joint potential of France

and Germany can be increased if the employees from both countries can

be motivated to work together.

Oddo considers the

German banking system as very strong and effective. This is mainly

because of the savings banks and cooperative banks. The reason for

the traditional capital market abstinence of the Germans sees Oddo in

the timidity against debt financing and poses at the same time the

question, whether the middle sized companies are really in need of a

capital market. In France, this topic is being considered much more

open. Oddo points out that between 2007 and today, the volume of the

capital market in Europe has shrunk by 40 percent, while in the same

period in the US an increase of 130 percent has taken place.

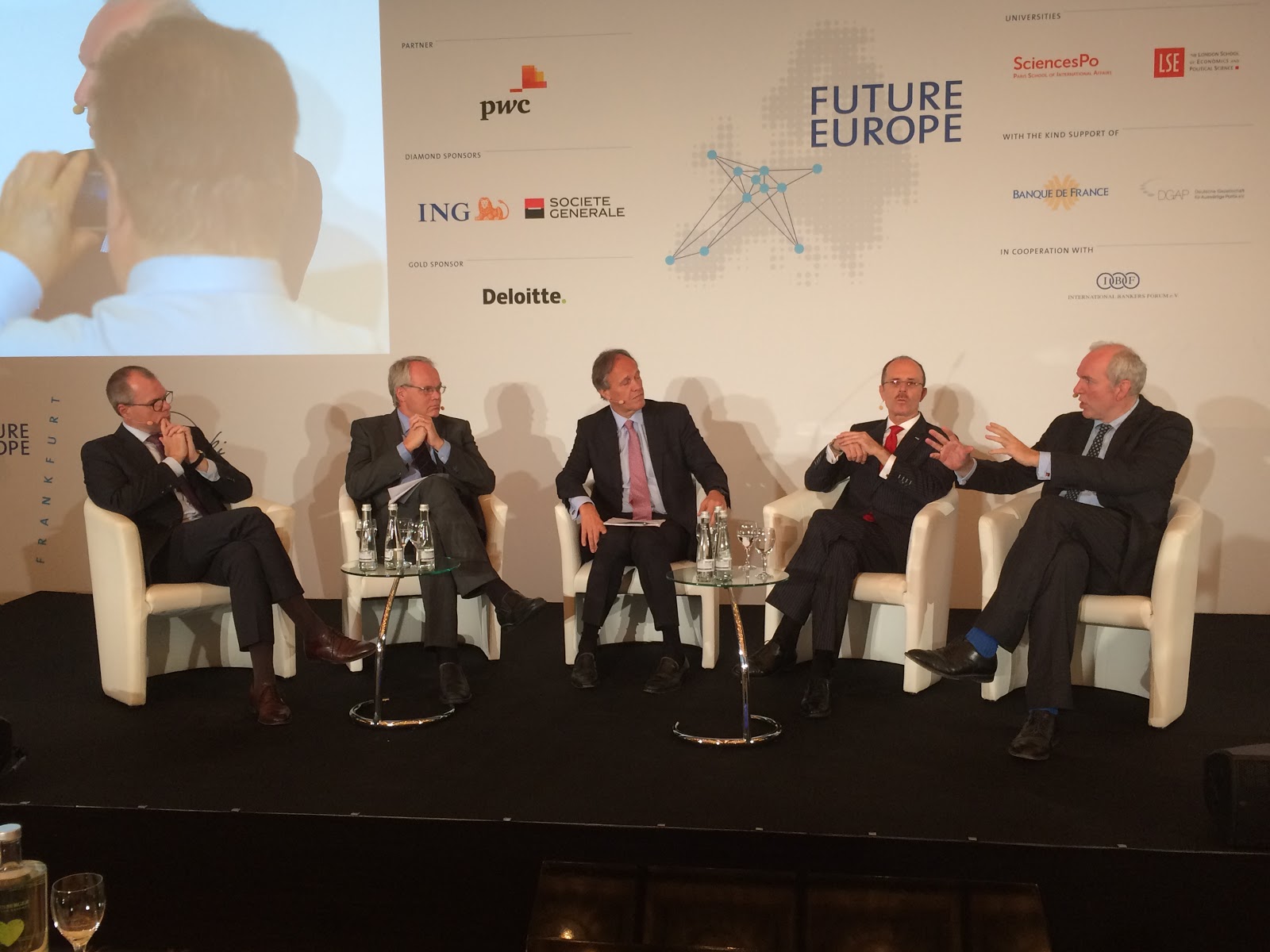

|

| The Frankfurt panel, left to right: Gerhard Schröck, Philippe Oddo, Stefan Collignon, Michael Rüdiger, Joachim Würmeling (Quelle: Thomas Seidel) |

Like Peter Praet,

Oddo sees the lack of a deposit insurance solution as the main

obstacle to European bank mergers. One can not use German deposits

for financing losts in other countries.

The acting

Bundesbank executive committee member Prof. Dr. Joachim Würmeling

explains that Europe's outward view has always been made by the

capital market in London, which is now being swept away by the Brexit

for Europe. Würmeling hopes that new technologies will help to

create a platform that will enable the dismantling of very fragmented

financial markets in Europe. Würmeling still sees the euro as the

common European currency in twenty years' time. At the moment there

is more than ample liquidity. But the supply of capital to some

countries in Europe could become more expensive as a result of

Brexit. In this case, Europe must take precautions.

Dr. Gerhard

Schröck of Deloitte stresses the importance of a recovery of the

European banking industry. After all, corporate finance depended for

more than half of bank loans. The establishment of the European

Banking Supervision SSM (Single Supervisory Mechanism) as a

recognized institution within just four years is a remarkable

achievement. Of course, the supervisor must now move more to a

qualitative approach based on the US model and not just pursue the

quantitative approach as before. This means that financial

supervisors need to better understand business models and the

complexity of doing business.

The second panel

on the same topic also included contributions from the video-linked

venues Paris London and Amsterdam.

Lorenzo Bini

Smaghi, the prevented ECB president and now chairman of the board of

the major French bank Société Generale, emphasizes the need for a

European capital market. At the same time he describes the obstacles.

There will be no capital market unless there were pan-European banks.

But that will not be possible without a European deposit insurance.

While in the US banks get bigger and bigger, there are too many

small-scale banks in Europe. For all this, Germany and France should

look ahead together and be oriented towards the USA. Then it needs a

schedule that one work through step by step.

|

| Crossing borders: Roland Boeckhout Amsterdam above left., Lorenzo Bini Smaghi Paris below leftl., Minouche Shafik London above right, Andreas Dombret below right (Source: Thomas Seidel) |

The Dutchman

Roland Boeckhout, board member of the Dutch ING Bank, is very

skeptical about the capital market. Europe simply lacks the knowledge

and skills. The skills are still in London. He laments the lack of

solidarity in Europe. There is a lack of objectification. At the

moment there are a lot of emotions in Europe but no European

solutions.

The president of

the German banking supervisory authority, Felix Hufeld, is surprised

that only a short time ago one had warned about too big banks "to

big to fail", but now speaking again of the necessity for

globally competitive banks. The problem in Europe is that there is a

lot of capital that is looking for profitable investments, but such

investments are hardly to find in Europe. Hufeld distinguishes

between supervision, which makes a daily work about supervision in

detail and the regulation, which he considers more as a political

task.

|

| Simultaneously in Frankfurt, from left to right: Felxis Hufeld, Andreas Dombret, Harald Kayser (Source: Thomas Seidel) |

Again and again,

the participants discuss the missing European capital market. Harald

Keyser, who will shortly head PwC Europe SE in Berlin, also

recommends reducing dependence on the London capital market. For

this, Europe needs more standardization and harmonization and less

competition between locations such as Paris, Amsterdam, Luxembourg

and Frankfurt. As a major obstacle, however, Keyser sees the

political decision-making emergency.

Strengthening the EURO-Zone

The next panel

focuses on strengthening the Eurozone. An introduction will be given

by the former Dutch Minister of Finance and Chairman of EURO Group

Jeroen Dijsselborn. For him, the most important homework is the

completion of banking and capital market union, but also to begin

with an improvement in labor markets and pension systems.

From the work in

the European Parliament Jakob von Weizsäcker reports. New European

projects should prove that they can make a difference step by step.

He gives an example of Frontex. Before any financing, it must be

clear what effect getting 10,000 more officials at the external

borders. But von Weizsäcker fears an end to the European project. In

more and more countries, the political orientation is to be only pros

or cons of the European Union. The awareness of the commonality is

fading.

In the typical

Prussian-Wilhelminian style ("the world should adopt the German

character") presented by the only governmental member of the

German Federal Government Thomas Steffen, State Secretary in the

Federal Ministry of Finance. For him, the mayor constraint is

currently the unsolved problem of a European deposit insurance. Many

other approaches, such as asylum policy, corporate taxation, etc. may

also be important, but the unsolved deposit insurance is currently

preventing everything in Europs financial markets. But of course, he

expects the only solution can be a German model and the repeatedly

demanded catharsis of bad loans.

|

| from left to right: Jörg Zeuner, Lüder Gerken, Stefan Collignon, Thomas Steffen, Jakob von Weizsäcker (Source: Thomas Seidel) |

The former

governor and current professor at the London School of Economics,

Lord Mervyn King, first lectures on the lost competitiveness of

Southern countries in Europe. They could not compensate by devaluing

within the euro. Therefore, there must be an internal devaluation,

but this would trigger high unemployment. Alternatively, one could

also promote inflation in Germany and the Netherlands, for example.

The third possibility would be to carry out transfers in Europe (the

German irritant theme par excellence). Anyway, it would inevitably

come to that. If one goes along this path without adequately

informing the electorate, it would only strengthen the right-wing

radical forces. Another problem is the lack of democratic legitimacy.

Under no circumstances should politics keep silent about the truth.

(Note: Is this a British insight from the Brexit vote?) Lord Mervyn

King then alleged with the statement: It is not Great Britain who is

leaving the European Union, but the EU is leaving Britain. Finally,

King explains the failure of the Brexit advocates. What they did not

do, was give a positive justification for remaining in the EU. They

only argued with the cost of leaving. But with such a statement you

could win no vote. Similarly, the EU should be able to communicate a

positive reasoning for Europe.

|

| from left to right: Christian Sewing, Stefan Collignon, Norbert Röttgen (Source: Thomas Seidel) |

Then the

concentrated pessimism about Europe spreads in the upcoming debate.

It comes to statements such as by the former Italian Prime Minister

Enrico Latta, in Europe there is currently either only "no"

or „nightmares“. Christina Sewing, the youngest head of Deutsche

Bank, sees a lack of negotiable visions for Europe. The German

parliamentarian Norbert Röttgen philosophizes that at the end of the

post-war period a new epoch has not yet begun. It is not clear which

order is now resulting. For a deep disagreement prevail. It would be

discussed different value, but one do not know which values will

prevail. That's why the role of the EU in the world needs to be

redefined, including the issue of migration. The President of the

Banque de France Francoise Villeroy de Galhau finally gives a sense

of a achieved banking and capital market union. It is about

transforming the 400 billion euros of private savings into

investment.

Conclusion

Once again, this

event has made it clear that the current inability of the European

Union to work together in a constructive and collaborative manner is

putting the project Europe at an ever faster and more fundamental

risk. More than ever, everything seems to be teeters on the brink.

Even though the banks seem to be pleading for the completion of the

Banking and Capital Markets Union, they are all unable to separate

internally from their national action cultures. This is even more

true for politics. Already the pro-European fire, which briefly

caused the French President Macron to blaze, again only a faint glow.

The hope for leadership and assumption of responsibility for Europe

by Germany shatters like a striking crystal glass because of an

absurd power dispute of a small regional people's party. The forces

of perseverance on national priorities are on the rise everywhere, if

not already on the march. This is how Europe crumbles itself or is

wiped out by global reality.

|

| Nader Maleki established a new conference format (Source: Thomas Seidel) |

Keine Kommentare:

Kommentar veröffentlichen