|

| A fully attended event 5th Capital markets day of bank Hauck & Aufhäuser in Frankfurt/Main (Source: Thomas Seidel) |

The semi-annual event of the

traditional bank owned by the Chinese Fosun Bank is addressed to

independent asset managers. Due to the continuing strong demand for

the event, there will be space for more than 270 participants. The

central lecture will be given by the President of the Munich ifo

Institute, Prof. Dr. Clemens Fuest. He is regarded as one of the most

renowned economists in Germany and is also a member of the Council of

Economic Experts. His statements on the development and progress of

economic activity in Europe are eagerly awaited.

The event will be introduced by Michael

Bentlage (CEO Hauck & Aufhäuser). Michael Bentlage can report a

positive business development for his company. Following Hauck &

Aufhäuser's acquisition of the Luxembourg activities of the former

bank Sal. Oppenheim, Bentlage has managed a smooth integration

without any fundamental impact on the processes in Luxembourg and

Germany. Hauck & Aufhäuser employs around 350 staff in

Luxembourg and manages around 80bn euros of assets at various levels

of the value chain. All business units operate profitably in their

own areas of focus. Hauck & Aufhäuser also sees itself well

positioned for the coming year.

|

| Michael Bentlage CEO Hauck & Aufhäuser (Source: Thomas Seidel) |

Global economic activity

Clemens Fuest

serves his role as a favourite for the core lecture. In a precisely

structured presentation, Fuest deals with currently important

economic topics. From the point of view of Fuest and the ifo

Institute, the traffic light is clearly yellow. The economic peak at

the beginning of 2017 is long over. The economy is experiencing a

considerable slowdown. In particular, the "uncertainty

indicator", determined by surveys of companies, has risen from

52 to 57.

The Trump administration is trying to

keep the US economy at this level until the next presidential

election. But the clear turnaround in interest rates and the

government deficit, which has risen sharply as a result of massive

tax cuts, raise doubts about this plan.

Fuest sees the trade dispute with the

US as ambivalent. It is true, that Europe has a trade surplus over

the US in goods. But the situation is quite different for services.

There the US is in the plus. Last but not least, large US companies

are making strong profits in Europe. The trade relationship between

the US and China is quite different. The Chinese sell services to the

US for 506 billion dollars, while the latter only supply China for

131 billion dollars. This would put the Chinese in a worse position

in the trade dispute. They simply run out of goods coming from the

US, which they could still impose customs duties on. So it is hoped

in Europe that the trade dispute will concentrate on China and the

US.

Fuest rightly omits the subject of

Brexit. New and sometimes contradictory information, virtually every

hour, is not a suitable basis for development forecasts.

|

| Prof. Dr. Clemens Fuerst ifo-Institute Munich (Source: Thomas Seidel) |

Fuest, on the other hand, is right in

its choice of Italy. It begins with positive facts. There would be an

economic recovery of just under two percent. The labour market is

running relatively well. There would be a surplus in the trade and

current account balance, as well as a primary surplus of just under

two percent. But youth unemployment would be 35 percent, compared to

6 percent in Germany. The national debt has reached a level of 130

percent of the gross national product. The dynamics of export

strength are now negative. Worst of all, however, is the decline in

labour productivity since 1990, which is still declining compared

with other European countries. One of the reasons for this is the

high number of family-run companies with a strong traditional

approach.

All these shortcomings would be

exacerbated by radical political change. What the current government

is doing is robbing itself of a better primary surplus. Without

enormous growth, however, Italy could no longer hold its own in the

long run. The targeted additional debt will not be spent on

investments, but on pensions. Investor confidence will be lost.

Ultimately, however, the EU cannot change this. The Union is a

community of sovereign states that do not really have to adhere to

Brussels guidelines. Only the reactions of the markets could perhaps

bring the Italian government to a change of course.

|

| The uncertainty is rising (Source: Thomas Seidel) |

Fuest gives concrete advice. Europe

must not reward populist blackmail. Other countries would have to

protect themselves against a crisis in Italy. Without saying how in

detail, this will probably only be possible with equity capital for

write-downs on Italian bonds and loans. The EU should enter into a

dialogue with Italy and promote initiatives that bring European added

value. For example, in migration and security policy, in the

expansion of European networks and in research funding.

Fuest assumes, that the EU will remain

a community of sovereign states. Under this premise, an overall

political concept is needed. Fuest criticises the idea of a Euro zone

budget as wrong. There would already be 260 billion euros available

in the EU, but not yet called up. In principle, any risk sharing must

be accompanied by more market discipline.

Controversial discussion

After this detailed analysis, a panel

discussion will take place in which Fuest and Michael Bentlage from

Hauck & Aufhäuser, Claus Döring, editor-in-chief of the

Börsenzeitung, Prof. Dr. Christoph Schalast from the Frankfurt

School of Finance an Management (FSFM), and Christoph Subbe, CEO of

Frankfurter Lebensversicherung will take part. The participants

engage in a heated discussion. Döring sees the stock market

shrinking by 25 percent in one year. Subbe warns of severe volatility

in the markets. Schalast regards Germany as the "lame duck"

in Europe and foresees a new chancellorship for the coming year. He

is also confident that Italy will get its act together again.

Bentlage countered Döring, that the markets would not collapse so

sharply. He believes that the European banks are now well positioned.

The regulators had developed refined and expanded mechanisms for

monitoring them. The poor performance of some German banks can be

traced back to the regulatory system, which affects their equity

capital and business models. Verbal fights are being fought over the

problem of Italy. Döring warns, that the exposure of banks in Italy

is not properly taken into account in the bank stress tests.

Schalast, who is a self-confessed Italian fan, at least for groovy

clothes and shoes, believes in an elegant solution to the Italian

problem. While Döring considers the ECB's possibilities regarding

Italy to be exhausted, Fuest believes the big question is how the

financial markets would react and what liquidity problems this would

lead to. Subbe doesn't believe in the big Italian crash that nobody

really wants to see.

|

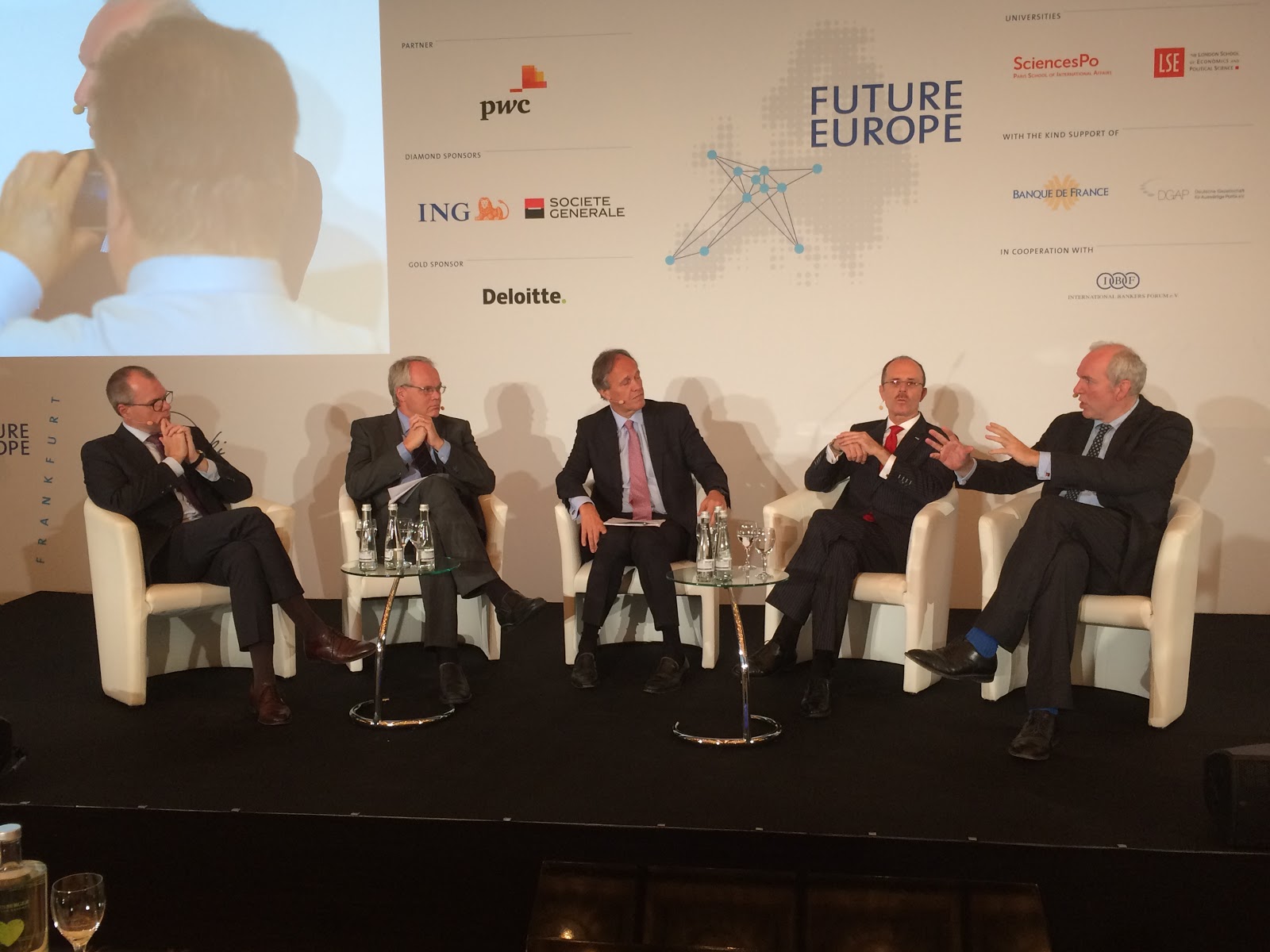

| Panel discussion (f.l.t.r.: Michael Bentlage, Clemens Fuest, Claus Döring, Christoph Schalast, Christoph Subbe |

In another issue Bentlage complains

about the handling of German cutting-edge technology. That would be

tantamount to selling out knowledge and human resources. Schalast

warns, that Germany is sealing itself off. Bentlage insists, that

competitiveness suffers. However, Döring does not regard

technologies as a national good. Fuest points out, that now, after

the globalisation of capital, the globalisation of goods is coming,

which is much more pervasive. He warns, that the key to the future is

the ability to set standards. This is the only way to ensure, that

the company's own products will be able to penetrate the markets in

the future.

In the event, which lasted barely three

hours, more substantial statements were made than in some major

events of the financial sector, which last several days. Hauck &

Aufhäuser has managed to bring important and interesting facts for

future economic events to the point for a closed audience. We will

continue to report on this exclusively.